What the rate update means

The Federal Reserve recently held its key federal funds rate steady after a series of cuts in late 2025, but signaled it may keep rates higher‑for‑longer into 2026. That means banks and lenders are likely to keep their borrowing rates elevated, which translates to higher interest on many forms of credit unless you lock in lower fixed‑rate deals. The Fed’s rate decisions don’t just affect Wall Street; they pass directly into the APR you see on credit cards, the rate you pay on a mortgage, and even the yield you collect on savings accounts.

Because the Fed’s benchmark rate influences the “cost of money” for banks, companies, and foreign investors, any change shows up in consumer products like credit‑card APRs, mortgage rates, auto loans, and savings yields. When the Fed keeps rates high or steady, lenders don’t feel pressure to cut what they charge borrowers, and they can still offer relatively attractive rates to savers. That’s why an interest‑rate environment set by the Fed can feel like a tectonic plate: it’s slow‑moving, but it shifts everything on the surface.

In practical terms, the latest update tells consumers that cheap money is still on hold. If you were hoping for lower borrowing costs on big purchases like a house or car, those hopes may have to wait. On the positive side, if you are a saver who shops around, you can still earn more on your cash than in the zero‑interest years of the early 2020s, especially in high‑yield savings accounts and certificates of deposit.

How it hits your credit card debt

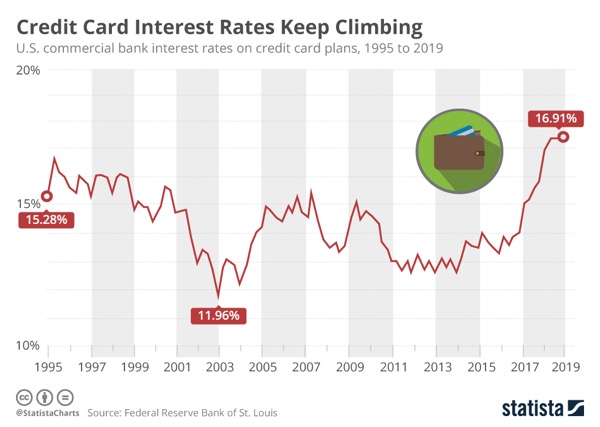

If you carry a balance on a credit card, the latest U.S. interest‑rate update could mean paying more in interest each month. Many credit cards tie their APRs directly to the prime rate, which is closely linked to the Fed’s target. When the Fed keeps its key rate high or steady, card issuers typically pass that cost on to cardholders, raising their effective interest without always warning them in advance.

Because most credit‑card APRs are variable, a single Fed decision can push your rate up within one or two billing cycles, especially if you’re already near the upper limit of your card’s rate range. For example, if your card was at 18% and the Fed’s move pushes the prime rate up, you might see your APR jump to 20% or even higher, depending on your card’s terms. That extra 2–3 percentage points can add hundreds of dollars in interest over time if you’re carrying a large balance.

High‑interest credit‑card debt becomes especially painful in this environment because every dollar you carry from month to month is costing more. If you’re only making the minimum payment, more of your money goes toward interest and less toward the actual balance. That makes it harder to get out of debt and easier to fall into a cycle where your total payoff time stretches longer and your total interest bill climbs higher.

Auto loans, personal loans, and Buy Now Pay Later

The rate update also affects auto loans, personal loans, and Buy Now Pay Later (BNPL) arrangements. If you’re financing a car purchase or a large personal loan, lenders base their rates on the current cost of money, which is influenced by the Fed. When interest rates are higher, auto‑loan APRs tend to climb, which can push your monthly payment up even if the sticker price of the car stays the same.

For people using variable‑rate auto loans or flexible financing plans, the impact can be even more pronounced. If your loan has a rate that adjusts over time, a Fed decision to keep rates elevated can trigger a reset that makes your monthly bill noticeably heavier. Similarly, some BNPL or “0% introductory rate” offers are built on the assumption that money is cheap; when the Fed tightens, lenders may start charging more for those programs or shorten the grace periods.

Before signing any new loan or financing agreement, it’s wise to read the fine print and ask whether the rate is fixed or variable. A fixed‑rate loan can protect you from future Fed moves, but sometimes comes with slightly higher upfront costs. A variable‑rate loan may look cheaper at first, but could become much more expensive if interest rates stay high or rise again.

Mortgages and housing costs

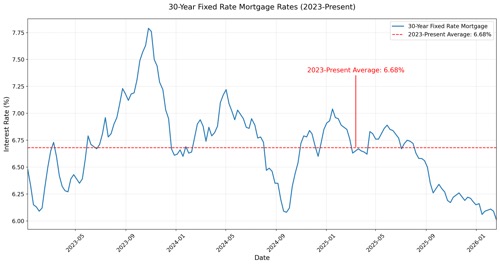

For homebuyers, the latest U.S. interest‑rate update can significantly change how much house you can afford. Mortgage rates typically follow the direction of the Fed and broader bond markets, so when the central bank keeps rates steady or moves them higher, home‑loan interest tends to stay elevated as well.

Many Americans are now seeing mortgage rates hovering in the mid‑6% range, which keeps monthly payments higher than in the ultra‑low‑rate years of 2020–2021. That means the same home can cost you more in interest over 30 years, or that you may have to aim for a less expensive house to keep your payment comfortable. For first‑time buyers, this can feel like a double squeeze: high home prices and high interest rates both eating into affordability.

Refinancing is another area where the rate update matters. If you locked in a low rate a few years ago, refinancing may no longer be as attractive, because the new rate might not be much better—or could even be worse—than what you’re already paying. If you’re considering refinancing, it’s worth comparing your current rate with today’s offers and estimating how long you plan to stay in the home, since refinancing involves closing costs that can offset savings if you don’t stay put long enough.

Savings, CDs, and banking rates

On the flip side, steady or elevated rates can help savers who shop around. High‑yield savings accounts and CDs may still offer yields in the 3–4% range, far above the near‑zero rates of a few years ago. That means emergency funds, savings buckets, and short‑term parking spots for cash can earn more interest without tying up money in riskier investments.

However, not all banks pass these higher rates on equally. Large traditional banks often keep savings rates low, while online banks and credit unions can offer much better yields. If you’ve left your savings in a brick‑and‑mortar checking or savings account, you might be leaving money on the table. Simply moving your emergency fund or a portion of your savings to a high‑yield account can boost your interest earnings without much extra risk.

For people who are risk‑averse or planning a big purchase in the next year or two, CDs can be a smart choice. Locking money into a CD at today’s higher rates means you guarantee a return for that term, even if the Fed later cuts rates. The trade‑off is less liquidity, but for money you don’t need right away, that trade‑off can be worth it.

Investments and retirement accounts

The rate update also affects investment behavior, especially for people with money in bonds, money‑market funds, or certain retirement accounts. When interest rates rise, bond prices tend to fall, which can temporarily hurt the value of bond funds. However, higher rates also mean new bonds offer better yields, so over time, bond investors may end up earning more as older, lower‑yield bonds are replaced by newer, higher‑yield ones.

For retirees or near‑retirees who rely on income from bonds or fixed‑income investments, the current high‑rate environment can be a double‑edged sword. Short‑term volatility may feel uncomfortable, but longer‑term income potential can improve as new bonds at higher coupons replace older ones. Anyone in or near retirement should think carefully about how much exposure they want to longer‑term bonds versus shorter‑term or more flexible options.

Stock investors may also feel the impact indirectly. Higher interest rates can make borrowing more expensive for companies, which can slow growth plans, reduce profits, or lead to layoffs. That, in turn, can shake stock prices and make markets more volatile. For long‑term investors, the key is usually to focus on diversification and time horizon, rather than reacting to every Fed decision.

Why this matters to everyday Americans

For ordinary Americans, this interest‑rate landscape means more pressure to pay down high‑interest debt fast, because cards and variable loans won’t get cheaper right away. Every dollar you pay toward high‑APR balances can save you far more in interest than it might have a few years ago, when rates were near historic lows. That makes aggressive debt repayment a strong strategy in this environment.

At the same time, steady rates create more reward for disciplined saving, especially in high‑yield accounts, but very little upside from traditional checking or savings at big‑name banks. If you’re not shopping around for better rates, you’re effectively leaving money on the table. This setup also makes it smarter to think twice before taking on new debt for non‑essential purchases, because borrowing for cars, vacations, or unplanned expenses can become costlier over time.

For middle‑income households especially, the combination of higher borrowing costs and modest wage growth can squeeze monthly budgets. Inflation has cooled somewhat, but higher interest rates still make it harder to stretch each paycheck. That’s why many financial planners recommend focusing on three areas: cutting high‑interest debt, locking in affordable fixed‑rate loans, and optimizing savings vehicles to capture the best available yields. Oil Prices Crash as Trump Pauses “Project Freedom” in the Strait of Hormuz

Smart moves to protect your wallet

To protect your wallet, experts commonly suggest focusing on three areas: reducing high‑interest debt, locking in affordable fixed‑rate loans, and parking emergency savings in higher‑yielding accounts. If you have credit‑card balances or a variable‑rate loan, consider moving money from high‑yield savings or negotiating a balance‑transfer card or fixed‑rate refinance to cut interest costs. Every dollar you free up through smarter borrowing can be redirected toward savings, investments, or paying down other debts.

Before taking on new debt—especially for big or flexible expenses—run the numbers with today’s higher rates in mind. Ask yourself whether the monthly payment still makes sense if interest stays where it is or even climbs a bit more. If the answer is no, it may be better to delay the purchase, save more first, or downsize your plan. For example, a smaller car, a less expensive home, or a shorter trip could keep your borrowing lower and your payments more manageable.

Finally, review your savings accounts and CDs regularly; if your current bank isn’t paying much, switching to a high‑yield option can turn this rate environment into a small source of extra income instead of a hidden drain. Even shifting a portion of your savings can make a noticeable difference over time, especially if you’re parking money that you don’t need for at least a year or two.

In short, if the Fed keeps rates steady or moves them higher, the smart move is to reduce variable‑rate debt, lock in affordable fixed‑rate loans where possible, and park emergency savings in higher‑yielding accounts to let this rate environment work for you instead of against you. By adjusting your habits now, you can soften the blow of higher interest to your wallet and even turn some of these changes into a small financial advantage.

Frenzy valentine is a passionate blogger, developer, and entrepreneur. He is the founder and author of myfreshgists.com.